- Daily Energy Market Update

- Posts

- Daily Energy Market Update March 9,2026

July 25, 2026

WTI is up $10.00 at $100.90 May RB is up 18.99 cents at $2.8862 ULSD is up 32.14 cents at $3.9438

Liquidity’s Daily Market Overview

Energy futures are much higher today as oil facilities in the Mideast are being targeted and several Mideast producers have been forced to shut in more output. As ING writes : "the situation appears to be deteriorating further." Yet, it is worth noting that the energies are well off their overnight highs as reports cite a possible release of oil reserves.

Iraq's oil production is down 70% to 1.3 MMBPD compared with a production level of 4.3 MMBPD before the war began. Output has been shut in as the country is unable to export oil via the Strait of Hormuz. "Crude storage has reached maximum capacity and the remaining output after the major cut will be used to supply the country's refineries," said an official with the state-run Basra Oil Company (BOC), which manages production and export operations from the southern fields. Iraq's exports also fell sharply to an average of around 800 MBPD on Sunday, with only two tankers loading because vessels cannot move freely through the strait to Iraq's southern terminals, the source said. Iraq’s oil exports from the southern oilfields stood at 3.334 MMBPD in February, as per Reuters reporting. Iraq relies on crude sales for nearly all public spending and more than 90% of its income.

Kuwait declared force majeure Saturday. (Reuters) Kuwait reportedly has cut output by as much as 300 MBPD. (ING) Shutting in an oil well risks long-term damage to reservoir pressure and incurs high restart costs, usually making it a measure of last resort. Restarting production can take days or even weeks depending on the reservoir. (WSJ)

Saudi Aramco has begun cutting output at two oilfields, two sources told Reuters. It was not immediately clear at which fields and by how much production was being curtailed. Storage is starting to fill up, as per Bloomberg reporting. A Kpler analyst says that Saudi Arabia is not cutting output, but that this is a reallocation of supply. “The reduction is happening in fields that do not produce Arab light grades which can be exported via the Yanbu terminal." Separately, a report from WSJ says a drone attacked a Saudi oil field (Al Berri that produces 250 MBPD)-although the WSJ report cites minor damage. Saudi Arabia intercepted drones that were heading toward the 1 MMBPD Shaybah oil field over the weekend. (Bloomberg) Saudi Arabia has directed a great deal of its crude for export to its Western ports. Shipments from its western terminals have surged to a rate of about 2.3 MMBPD so far this month, ship-tracking data compiled by Bloomberg show. While that’s about 50% more than the kingdom has shipped from Red Sea in any month since the end of 2016, it’s far below the 6 MMBPD that the country has exported from the Persian Gulf in recent months.

G7 finance ministers, in an emergency meeting on Monday, will discuss a possible joint release of petroleum from reserves coordinated by the International Energy Agency. Three G7 countries, including the US, have so far expressed support for the idea, according to the people familiar with the talks. The meeting to be held is set to start at 8:30 AM. One person said some US officials believe a joint release in the range of 300-400 MMBBL — 25 to 30 per cent of the 1.2 billion barrels in the reserve — would be appropriate. (Financial Times)

On Sunday, US Energy Secretary Wright said that the oil market is currently pricing in a fear premium that won’t last. The war will only temporarily disrupt markets and ship traffic, and the timeline for things to normalize “in the worst case” is weeks, rather than months, he said on CNN. For shipowners and charterers operating in the region, however, the cost of insurance is not the major concern holding up traffic. Instead, they worry about the safety of vessels and crew, and say they would need full naval escort — along the lines of Operation Prosperity Guardian, a coalition to safeguard shipping in the Red Sea — or preferably an end to hostilities. (Bloomberg)

The Strait of Hormuz isn't closed because of missiles. It's closed because insurers pulled the plug, as per one comment. Protection and indemnity coverage for the strait vanished on March 5. That single move turned a war zone into a no-go zone for commercial shipping. No Protection & Indemnity insurance means no port entry, no canal transit, no financing. (Supply Signal) The US announced on Friday that it would roll out maritime reinsurance for the Persian Gulf region. The facility will cover losses up to about $20 billion “on a rolling basis”, according to a statement. (Bloomberg)

Retail fuel prices in the US have risen further today. Gasoline at the pump is averaging $3.478 today, as per AAA data. Since Friday February 27, before the Iran conflict began, the gasoline price average has risen by 49.6 cents. The diesel price average at the pump today is $4.656. That is up 89.9 cents since Friday February 27.

For analysts at ING, the base case is now four weeks of disruption to oil supplies— two of full upheaval and two weeks of 50%. The bank’s most dramatic scenario is a three-month, full disruption to oil and liquefied natural gas flows. This would likely see oil prices spiking to records through the second quarter, the bank’s analysts wrote in a note. (Bloomberg)

The monthly oil reports from the EIA, OPEC and IEA are to be released this week. The EIA's STEO will be released tomorrow Tues. 3/10. OPEC's report is due out Wednesday 3/11 and the IEA's monthly oil market report is set for release Thursday 3/12.

Energy Market Technicals

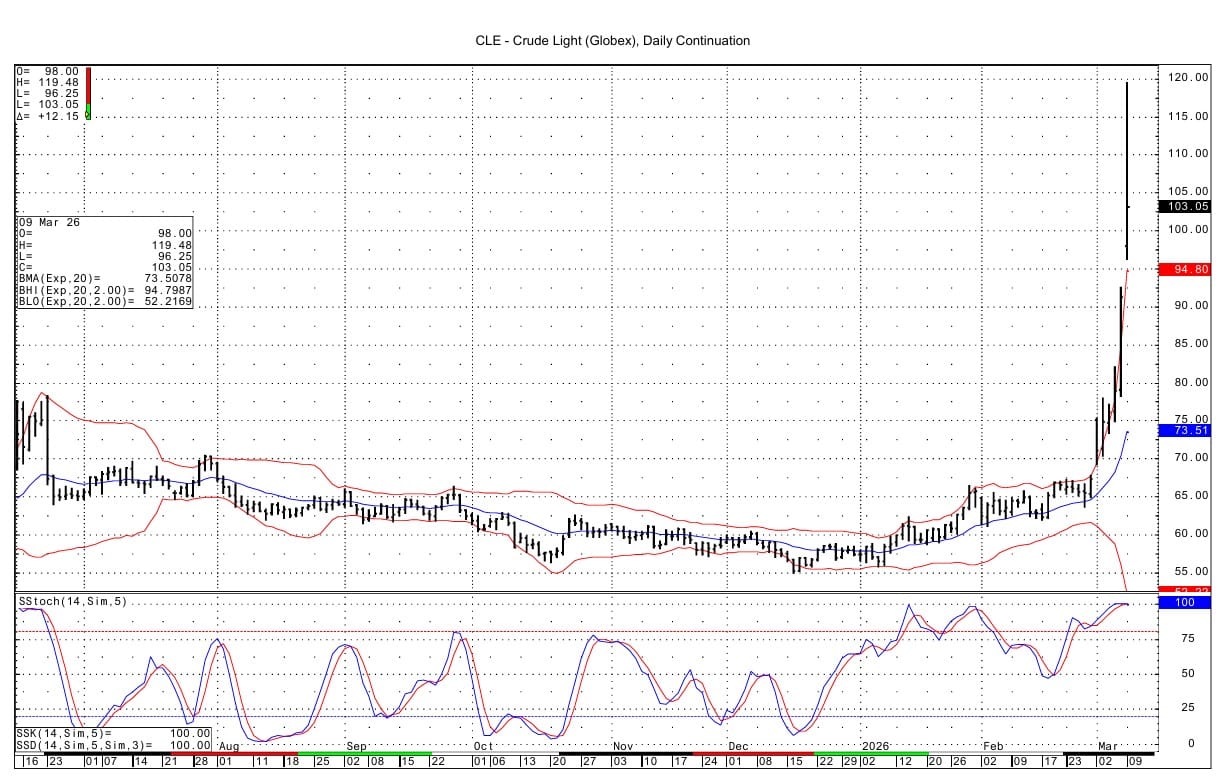

Momentum is overbought for the energies as they yet again test their upper bollinger bands.

WTI spot futures have resistance at 111.18-111.24 and then at the overnight high at 119.48. Support is seen at 96.25 and then at 92.51-92.61. The DC chart's upper bollinger band intersects at 94.95.

May RB futures have support at 2.7745 and then at 2.7142-2.7164. Resistance lies at 3.0413-3.0415 and then at the overnight high at 3.1468. The upper bollinger band on the daily May chart lies at 2.8102.

April ULSD futures support is seen at 3.7821 and then at the filling of the gap at 3.7485. Resistance comes in at 4.2200-4.2252 and then at 4.3799-4.3822. The overnight high lies above that at 4.4715. The DC chart's upper bollinger band lies at 3.9304.

Natural Gas Market Overview

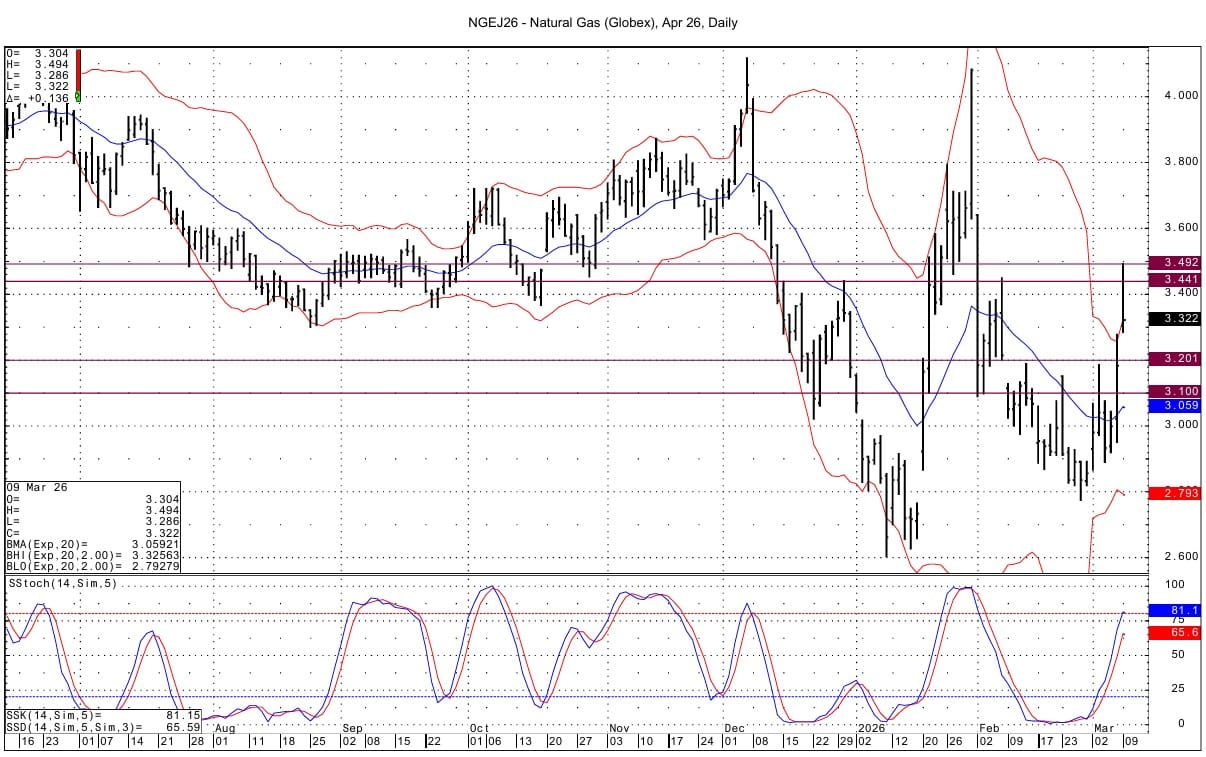

Natural Gas--NG is up 12.4 cents at $3.310

NG futures have also gapped up over the weekend as the Iran conflict has given this commodity a boost as well.

US weather demand though is seen low in the coming days as we enter the shoulder season, but set to rise thereafter. NatGasWeather sees demand as low to very low in the day 1 through 8 period. Days 9 trough 13 are seen as having moderate to high demand. Then days 14 and 15 show low demand. But, the NOAA raised their HDD count to above normal for both the 6-10 day and 11-14 day periods at 98.48 (18 above) and 64.85 (4.22) above, respectively.

The TTF European gas futures have gapped up this morning on the back of the ongoing tension/disruptions in the Mideast. The spot futures gap goes from Friday's high of Euro 53.835 to today's low of 59.545. Technically, the spot futures are trading above the DC chart's upper bollinger which lies near 58 Euros. The contract is not overbought basis the DC chart's momentum indicator. Today's high of Euro 69.500 was the highest spot futures price seen since early January 2023.

Lower 48 states dry gas production was estimated up at 114.16 BCF/d yesterday compared to a 30-day average of 113.69 BCF/d, BNEF data shows.

Money managers did not change their positioning in NG futures/options on the CME in the week ended Tuesday March 3. They remained net short a total of 75,910 contracts.

WSJ commentary regarding NG pricing reads as follows:" Futures prices for autumn gas deliveries suggest that traders expect adequate inventories and relatively low prices for the power-generation and heating fuel to persist through summer." The October 2026 January 2027 spread has widened the past 2 days to its greatest value for the January contract versus the October. Commentary seen suggests that this is more about concerns of an increase in LNG export demand come next winter.

The gap created over the weekend in NG futures lies from 3.280 to 3.286. Support below is seen at 3.201-3.202 and then at 3.099-3.100. Resistance lies at 3.436-3.442 and then at the overnight high at 3.490-3.494. NG futures have positive momentum that it not yet overbought basis the DC and April daily charts. The April daily chart though is seeing its upper bollinger band being tested today. The band lies at 3.320.

Enjoyed this article?

Subscribe to never miss an issue. Liquidity’s Daily Energy Market Updates provide a comprehensive analysis of both the fundamentals and technical factors driving energy markets.

Click below to view our other newsletters on our website:

Disclaimer

This article and its contents are provided for informational purposes only and are not intended as an offer or solicitation for the purchase or sale of any commodity, futures contract, option contract, or other transaction. Although any statements of fact have been obtained from and are based on sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed.

Commodity trading involves risks, and you should fully understand those risks prior to trading. Liquidity Energy LLC and its affiliates assume no liability for the use of any information contained herein. Neither the information nor any opinion expressed shall be construed as an offer to buy or sell any futures or options on futures contracts. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Any opinions expressed herein are subject to change without notice, are that of the individual, and not necessarily the opinion of Liquidity Energy LLC

Reply