- Daily Energy Market Update

- Posts

- Daily Energy Market Update March 12, 2026

July 28, 2026

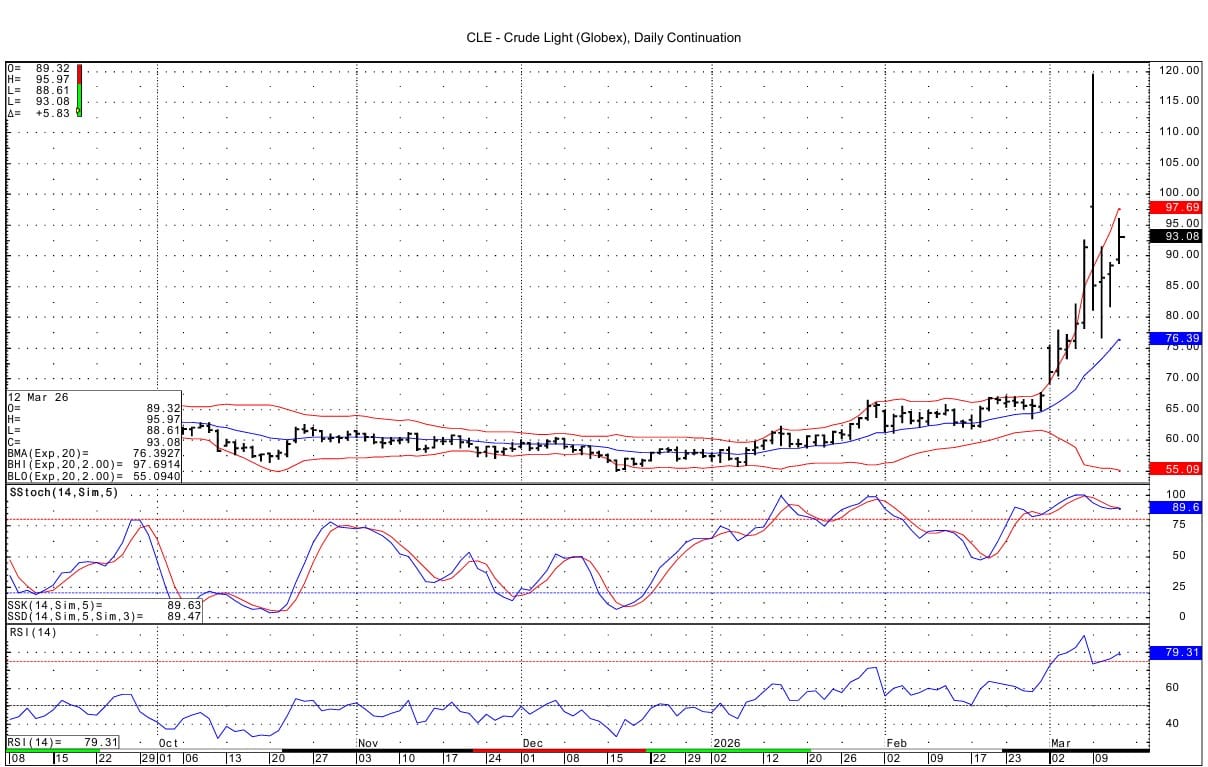

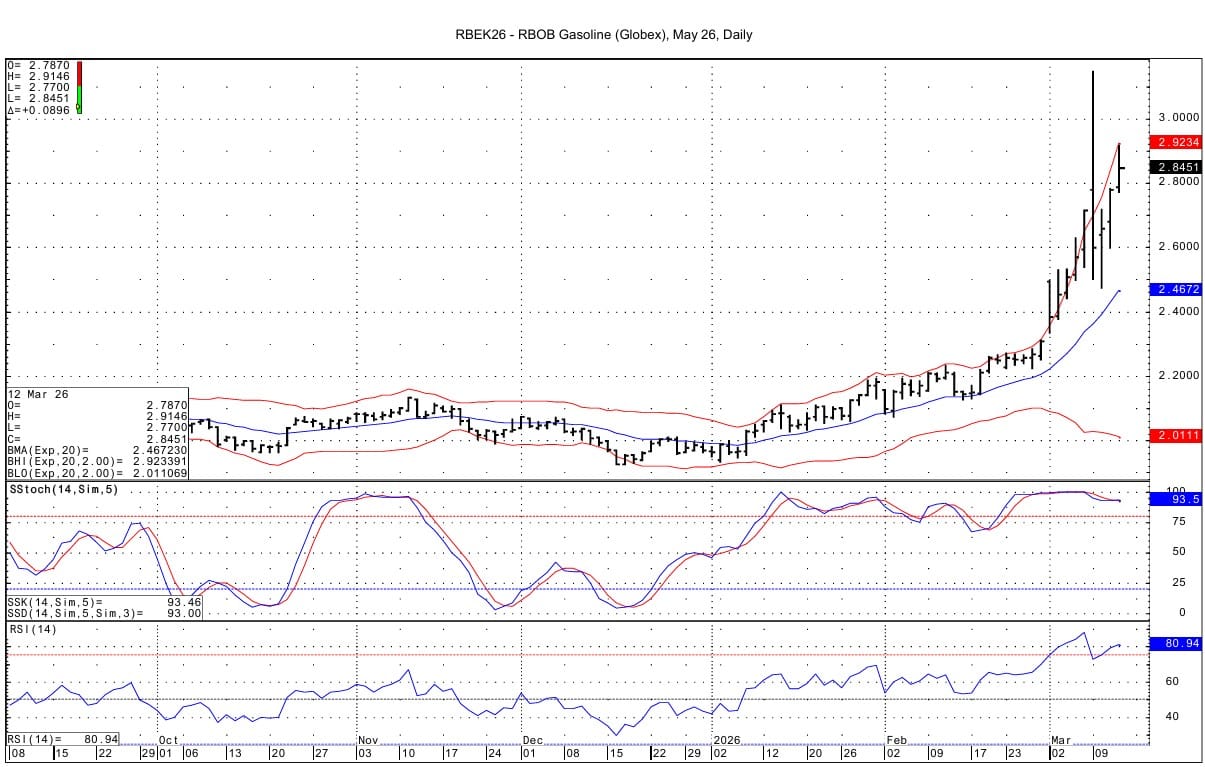

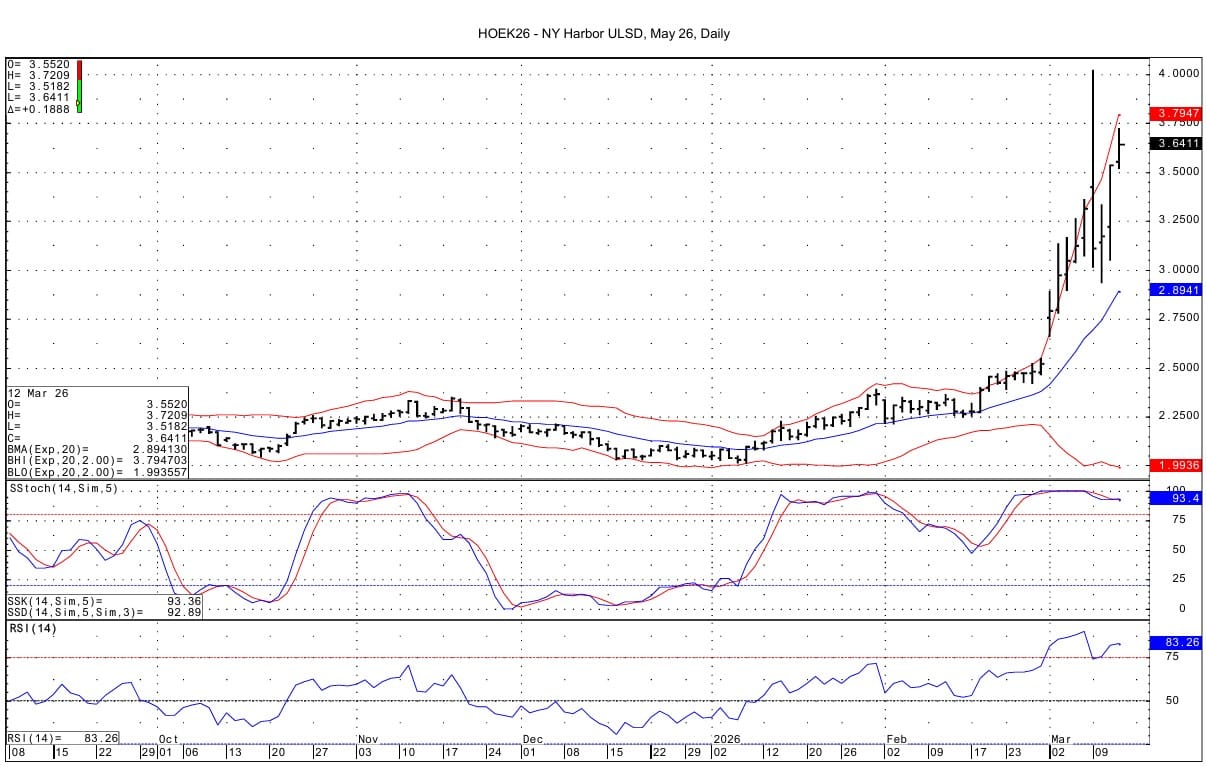

WTI is up $6.85 at $94.10 May RB is up 11.38 cents at $2.8002 May ULSD is up 21.95 cents at $3.6718

Liquidity’s Daily Market Overview

Energies are higher as the market has shrugged off the very large oil reserve release announced Wednesday by the IEA. Hopes for quickly reviving trade through the Strait of Hormuz are dimming without U.S. naval escorts as Iran steps up its attacks on shipping. Brent spot oil futures rose at their high over $100 today. "The war in the Middle East is creating the largest supply disruption in the history of the global oil market," the IEA said in its report on Thursday.

Over the past day, Iran has struck three cargo ships attempting to transit Hormuz, and three other vessels were hit elsewhere in the region. And Iran's semi-official Fars News Agency said allied militias could block another key passage for ships in the Red Sea. (WSJ) And today, two tankers were ablaze in an Iraqi port after a hit by suspected Iranian explosive-laden boats. Early Thursday, a container ship was hit with a projectile off the coast of Dubai. More drones were reported on Thursday flying into Kuwait, Iraq, the UAE, Bahrain and Oman. (Reuters)

The IEA, in its monthly oil report issued today, slashed its forecast for oil-supply growth this year. The IEA now expects supply to grow by 1.1 MMBPD this year, down from 2.4 MMBPD previously. Supply in March is expected to drop by 8 MMBPD to 98.8 MMBPD, which would be the lowest level since the first quarter of 2022. Middle East Gulf countries including Iraq, Qatar, Kuwait, the United Arab Emirates and Saudi Arabia have cut total oil production by at least 10 MMBPD as a result of the conflict, the IEA said, adding that without a rapid restart of shipping flows these losses were set to increase. But, the IEA however, says that supply could rise in April as some Middle East Gulf producers use alternative export routes to bypass the Strait of Hormuz, and said that, for the year, production would still expand more quickly than global demand. Yet, the IEA adds that shut-in upstream production will take weeks and, in some cases, months to return to pre-crisis levels. The IEA sees world demand in 2026 rising by 640 MBPD, down 210 MBPD from the previous forecast. Overall, the IEA forecasts imply that supply will be higher than demand by 2.46 MMBPD in 2026, a reduction from a 3.73 MMBPD surplus in last month’s report. (WSJ/Reuters) More than 3 MMBPD of refining capacity in the Mideast Gulf region has already been shut due to attacks and a lack of viable export outlets, the IEA added in their monthly report today.

On Wednesday, the IEA agreed to release 400 MMBBL of oil, the largest such move in its history, to try to rein in crude prices. The IEA said the release had been backed unanimously by 32 member countries. But, the market shrugged off the IEA's announcement; Reuters commentary read : " supply fears persist". But releasing the reserves will take months, and account for just three weeks of supply from the blockaded strait, as per Reuters commentary.

Goldman Sachs analysts hiked their price forecast citing longer disruption to flows through the Strait of Hormuz. They now assume 21 days of low oil flows, up from a previous estimate of 10 days. The analysts now expect Brent prices to reach $71 a barrel, and WTI $67 barrel in the fourth quarter, up from $66 and $62 in their 10-day disruption scenario. If the disruption lasts 60 days, Brent will trade at $93 a barrel in the fourth quarter, and WTI at $89, they added. (WSJ)

Iran's President suggested online Thursday that for the war to end, the world would need to recognize Iran’s “legitimate rights,” pay reparations and offer guarantees against future attacks. (Reuters)

The US Energy Secretary said Wednesday that the U.S. would release 172 MMBBL of oil from the country's SPR. He said the release would begin next week and take about 120 days to deliver. (WSJ) Japan will release about 80 MMBBL of oil from its strategic reserves, equivalent to 45 days of supply. Japan will tap its reserves in coordination with the G7 and the IEA but will begin releasing its part from March 16, ahead of the IEA-led release. Japan's planned release will be part of the total IEA coordinated release of oil reserves, a Japanese Economy ministry official said. Bloomberg reporting says that Japan boasts strategic oil stockpiles equivalent to 254 days of total consumption. Japan is dependent on the Middle East for around 95% of its oil supplies and gets around 90% of its oil shipments via the Strait of Hormuz. (Reuters)

In Japan, the government will implement measures to keep gasoline prices at around ¥170 per liter, by using existing funds that were set up in the past to keep the fuel price from rising, she said. The nationwide average is currently at ¥161.8 per liter. In the US, the retail prices of gasoline and diesel have risen again in the AAA data. The national pump price for gasoline rose today by 2.0 cents to $3.598 and is thus up 61.6 cents since February 27. The price for diesel at the pump rose today by 3.0 cents to $4.860 and is thus up $1.103 since February 27.

Wednesday's DOE data showed a build of 3.824 MMBBL in crude supplies. This increase was largely a function of the increase in net crude imports on the week of 661 BPD (= 4.627 MMBBL). The net crude import increase was offset somewhat by the increase in crude inputs to refineries of 328 MBPD. Cushing oil supplies, at 26.6 MMBBL, rose to their highest level since August 2024, as per Market News analysis. Product demand rose on the week and is greater in this week's data than in the prior 2 years for this period in both gasoline and distillate. Gasoline demand rose on the week by 949 MBPD to 9.241 MMBPD---beating the prior 2 years demand by 59 and 197 MBPD. Market News commentary said that gasoline demand this week rose by the most in almost a year. Distillate demand rose on the week by 367 MBPD to 4.065 MMBPD ---beating the prior 2 years demand by 167 and 690 MBPD. The strong demand in gasoline was seen due to some degree to stockpiling due to the Iran war.

Energy Market Technicals

The rally of the past 24 hours has seen the stochastic momentum indicator for the energies turn neutral. But the RSI indicator for the energies has risen back to an overbought condition.

Spot WTI futures see resistance at 97.19-97.38 and then at 100.62. Support lies at 88.61-88.63, which is the overnight low. Support below that lies then at 84.67-84.70.

May RB support lies at 2.7700-2.7711, which is the overnight low and then at 2.7128-2.7142. Resistance is seen at 2.9164-2.9183 and then at 2.9697-2.9710.

May ULSD support is seen at 3.5882-3.5896 and then at the overnight low at 3.5182. Resistance above comes in at 3.7120-3.7121. The overnight high is 3.7263. Above that resistance is then seen at 3.800.

The spot Brent futures have gapped higher today---with the gap going from $93.80 to $95.20.

Natural Gas Market Overview

Natural Gas--NG is up 2.3 cents at $3.232

NG futures are up slightly as the Iran conflict and the prospect of cooler air have supported NG the past 24 hours. Celsius Energy analysis is calling for strong gas storage pulls over the next several weeks as a late-season shot of arctic air is expected. But, today's EIA gas storage data though is seen below average.

The EIA gas storage data due out today is seen as a draw of 46 BCF, as per the WSJ survey. That compares to last year's draw of 62 BCF and the 5 year average draw of 64 BCF. The lower than average draw for this week is seen due to a sharp fall in heating demand seen last week. This saw electrical gas-fired power generation fall. Gas-fired consumption may have been even lower had it not been for a 14% decline in power output from wind last week, NGI commentary read.

The NOAA forecasts the next 2 weeks to see below average temperatures in the Eastern half of the US, while the Western half will see above normal temperatures. An early-season heatwave across the Southwest and Deep South late next week could even support GWDDs, Celsius Energy says. Houston is set, in a week's time, to see temperatures rising into the mid-80's, which is 10 degrees above normal.

Celsius Energy analysis sees natural gas inventories having peaked potentially for the next month yesterday at 1871 BCF. Daily withdrawals return today and will peak early next week as a late-season shot of arctic air could push draws to -25 BCF/d, driving inventories to a seasonal nadir near 1780 BCF. That is below the EIA end March forecast for storage to be at 1.842 TCF.

There were several sizable options positions that were opened on the CME from Wednesday's activity. The April through October strip saw the $8.25/$8.75 call spread trade 0.7 cents. Open interest in those options rose by nearly 15,000 contracts across the entire strip. The October January CSO minus 75 cent/ minus 50 cent call spread traded in a 1 by 2 ratio at a flat price. The October January minus 50 cent call also traded against the minus $1.00 call in a 2 by 1 ratio at a cost of 5.5 cents to the -$1.00 call buyer. In the October January 3 month CSO, the minus $1.00 call and minus 75 cent call saw open interest rise by about 10,000 contracts, while the minus 50 cent call open interest rose by over 16,000 contracts. The October January futures spread settled Wednesday at -$1.432. In the July $3.25/$3.00/$2.75 put butterfly, over 6,000 butterflies traded between 2.8 and 2.9 cents.

Technically April NG futures have positive momentum. The market has rejected a move below $3, which was tested 2 days ago. Overnight resistance at $3.280 was tested. Above this, resistance comes in at $3.379-3.385. Support is likely at 3.099-3.100 and then at 3.019-3.025.

Enjoyed this article?

Subscribe to never miss an issue. Liquidity’s Daily Energy Market Updates provide a comprehensive analysis of both the fundamentals and technical factors driving energy markets.

Click below to view our other newsletters on our website:

Disclaimer

This article and its contents are provided for informational purposes only and are not intended as an offer or solicitation for the purchase or sale of any commodity, futures contract, option contract, or other transaction. Although any statements of fact have been obtained from and are based on sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed.

Commodity trading involves risks, and you should fully understand those risks prior to trading. Liquidity Energy LLC and its affiliates assume no liability for the use of any information contained herein. Neither the information nor any opinion expressed shall be construed as an offer to buy or sell any futures or options on futures contracts. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Any opinions expressed herein are subject to change without notice, are that of the individual, and not necessarily the opinion of Liquidity Energy LLC

Reply