- Daily Energy Market Update

- Posts

- Daily Energy Market Update January 23,2026

August 4, 2026

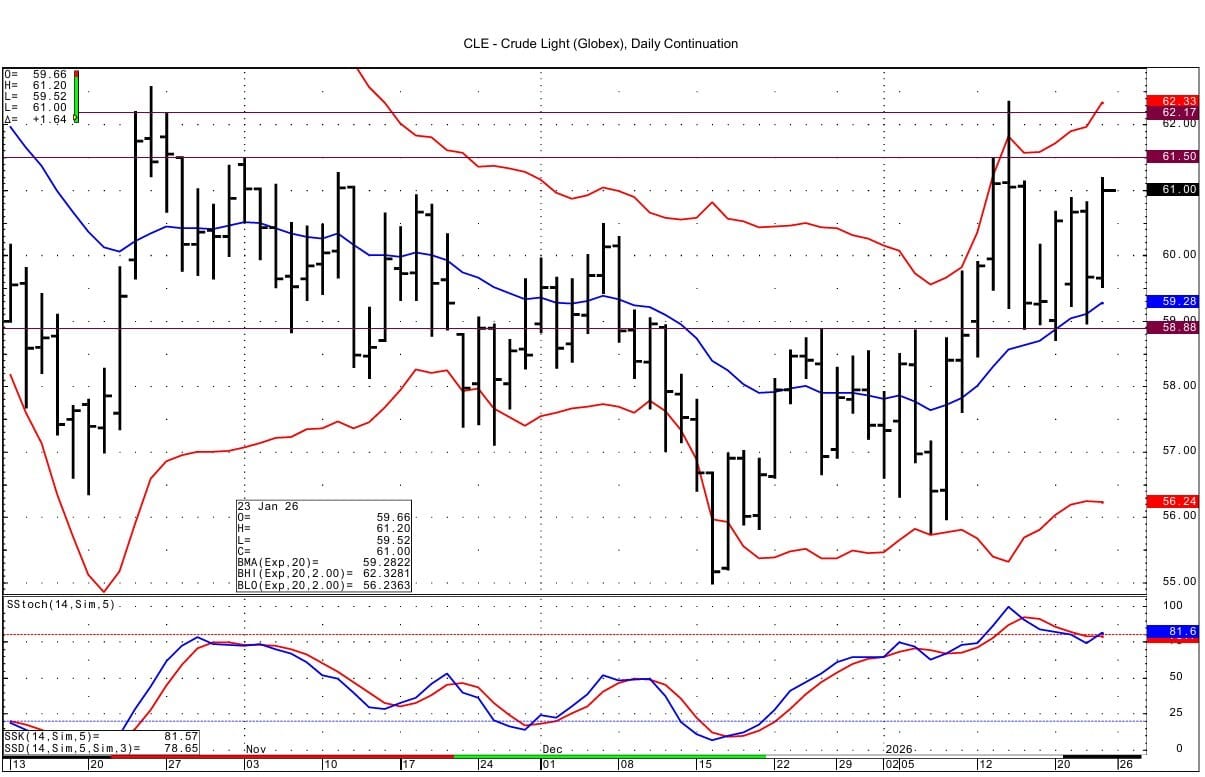

WTI is up $1.64 at 61.00 March RB is up 3.07 cents at $1.8694 March ULSD is up 4.18 cents at $2.3403

Liquidity’s Daily Market Overview

Energies are higher with Iran in focus as President Trump has renewed threats against Iran. Also, the continued outage of production In Kazakhstan is seen supporting prices. A weaker US dollar is also supportive. A headline out a few minutes ago has further boosted oil prices: US THREATENS CURBING SUPPLY OF CASH FOR IRAQ OIL SALES: Financial Times

President Trump said that the" U.S. has an "armada" heading towards Iran but hoped he would not have to use it, renewing warnings to Tehran against killing protesters or restarting its nuclear program." Warships including an aircraft carrier and guided-missile destroyers will arrive in the Middle East in the coming days, a U.S. official said. (Reuters)

Oil production at Kazakhstan's vast Tengiz oil field, one of the world's largest, has not resumed since its operator announced a shutdown on Monday, a spokesperson for Chevron, which owns 50% of Kazakh oil producer Tengizchevroil , said on Friday. JP Morgan said on Friday that Tengiz, which accounts for nearly half of Kazakhstan's production, may remain offline for the rest of the month, which would be in line with the estimates seen for production to be offline for 7-10 days. JP Morgan adds that Kazakhstan's crude output is likely to average only between 1 and 1.1 MMBPD in January, compared with a usual level of around 1.8 MMBPD.

Investing.com commentary today reads:" crude was headed for a fifth straight week of gains, amid expectations of improving demand and as markets priced in a greater risk premium on potential supply disruptions from heightened global geopolitical tensions." Investing.com cited improved Chinese growth data seen this week and the IEA raising their demand forecast slightly in their monthly oil report seen this week. US dollar weakness this week is also cited as a supportive element. The dollar is poised for its worst week since June, as per Bloomberg reporting. The Bloomberg Dollar Spot Index fell to a three-week low on Friday and is down 0.8% over five days.

Thursday's DOE data was slightly disappointing as supplies rose more than forecast and the supply increases for distillate and crude were greater than seen in the API data. The crude oil stockpile increase is largely due to the drop in crude input to refineries of 354 MBPD on the week---offset marginally by the lower US Crude production -down by 21 MBPD and the drop in net crude imports of 27 MBPD. Product demand fell on the week both for distillates and for gasoline --and each of them has lower demand this week than seen in the prior 2 years figures. Distillate demand fell by 572 MBPD to 3.524 MMBPD--less than the prior 2 years by 584 MBPD and 260 MBPD. Gasoline demand fell by 470 MBPD to 7.834 MMBPD--lagging the prior 2 years demand by 252 and 46 MBPD. US Gasoline Inventories Rise to Highest Since 2021 --Gasoline inventories are now at the highest level since 2021 and the highest seasonal level since 2020. (Bloomberg)

Energy Market Technicals

Technically, the WTI DC chart based momentum has turned positive, although the price pattern of the past 10 days has a more sideways look. The energies are currently having inside trading sessions versus yesterday's price range. The RB & ULSD momentums are trying to stay positive basis their March daily charts.

WTI spot futures resistance at 60.89-60.91 has been pierced in the last few minutes. Next resistance is at 61.50. Support lies at 58.88-58.96.

March RB support lies at 1.8261-1.8276. Resistance lies at 1.8808-1.8824. There is a double top from Wednesday/Thursday at 1.8800-1.8820.

March ULSD support lies at 2.2835-2.2851. Resistance at 2.3420-2.3432 has been tested this morning. Next resistance is then at 2.3678.

Natural Gas Market Overview

Natural Gas---February NG is up 14.8 cents at $5.193

Volatility remains very much in evidence today as the spot futures fell overnight by as much as 99 cents from yesterday's high of $5.65. The spot futures then rebounded back over $5.00, and are now trading up versus Thursday's settlement and are near the high for the session as we write. As one commentary reads:" Frigid weather across the U.S. is causing natural-gas prices to rocket higher, and could keep them elevated for days." But, the early February weather outlook was said to have moderated some, which led to the pullback off of the high seen Wednesday.

U.S. lower 48 states dry gas production is estimated today to be down 1.34 BCF/d at 109.53 BCF/d, compared to the 30-day average of 112.99 BCF/d, BNEF shows. At present, the cold weather in Texas has not yet impacted production in the Permian basin, but Market News writes :" Shut-ins are likely to increase through the day and into tomorrow as temps fall." Market News estimates Permian gas production could fall 3-4 BCF/d at its peak, and North Dakota gas production could fall 2 BCF/d. Wood Mackenzie estimated 9 BCF/d of Lower 48 shut-ins at their maximum between Jan 24-25 on Tuesday and Energy Aspects latest update calls for 4.5 BCF/d of outages over the next 2 weeks.

Average lower 48 states temperatures are forecast to drop well below normal into this weekend and hold until the end of the month before a gradual recovery back towards normal during the first week of Feb., as per NOAA readings. Forecasts point to prolonged, severe cold lasting into early February, with temperatures projected to fall as much as 37% below normal at their peak. (Market News)

The EIA gas storage data seen Thursday showed a draw of 120 BCF, which was 14 to 17 BCF more than the Reuters and WSJ survey estimates. Total gas in storage fell to 3.065 TCF. This was 141 BCF (4.82%) more than seen a year ago and was +177 BCF/ +6.13% versus the 5 year average. But, Celsius Energy sees the next 3 weeks data reducing the year ago surplus by 229 BCF and the surplus to the 5 year average by 305 BCF, thus turning both surpluses into deficits.

LSEG data seen Thursday forecasts this week's demand at 152.4 BCF/d, rising next week to 162.1 BCF/d. These forecasts were down a total of 4.3 BCF/d from those issued Wednesday. (Reuters)

As might well be expected given the volatility seen of late in the futures, the NG/LN options have seen heavy trading. The March 2026 call open interest rose by 25,325 contracts in Thursday's trading. Notable increases were seen in the $4.00, $5.00, $6.00 and $7.00 strikes. Among trades seen in the March calls, The $4/$6 call spread went in a 1 by 2 ratio at a cost of 9.4 cents with .12 delta futures sales at $3.56. The March $4.00/$5.00 call spread traded 13.5, 15.3 and 15.5 cents. The March $4/$5/$6 call butterfly traded 9.25 cents. The March $6.00 call traded 10.25 cents with .14 delta sales at $3.67. The March $7.00 call traded 6.0 cents with .09 delta futures sales at $3.54. February put open interest rose by 36,522 contracts in Thursday's activity. Among trades seen was the February $4.70/$4.30/$4.10 put fly in a 1 by 3 by 2 ratio. The cost to the buyer of the wings was 5.7 cents. The February $4.50 put traded 9.2 cents with .12 delta futures buys at $5.58. The February $5.00 put was bought at a cost of 24.8 cents with .26 delta futures buys at $5.55. In the LN/NG CSO's, notably the April October minus 25 cent call traded 4.4 and 4.5 cents. The April October spread settled Thursday at minus 45.3 cents. The October January -$1.25/-$1.50 put spread traded 3.8 cents. Thursday's settlement for the October January spread was -$92.7 cents. In the March April 1 month CSO, the flat put open interest rose by 9,500 contracts; among the notable trades was the selling of the flat put against which the +50 cent call was purchased at a cost of 5.3 cents. The March April NG futures spread settled Thursday at + 10.5 cents.

TTF options also traded actively on the CME Thursday. The Euro 32 put was bought against selling the Euro 29 and Euro 26 puts at a cost of .575 Euros. Additionally this trade saw .14 delta futures buys in March TTF at Euro 36.25. Today the March TTF is trading Euro 36.730. The April through September strip saw the Euro 25 put bought at a cost of 3.65 Euro with 0.4 delta futures buys at Euro 25.50. Also, the October 2026 through January 2027 strip saw the Euro 30 put trade Euro 3.825 with 0.47 delta futures buys in the strip at Euro 30.50.

Technically the NG spot futures have been repelled from near $5.65 for now. There is a double top from Thursday's high of $5.650 and the high from December 22, 2022 of $5.653. Above that, data from late 2022 shows resistance is possible at 5.890-5.906 and then at 6.250-6.273. Support lies at 4.871-4.878 and then at 4.688-4.696, which was tested with the overnight low of 4.66. The spot futures have also been repelled from the test seen the past 2 sessions of the DC chart's upper bollinger band. That band lies today at $5.375.

Enjoyed this article?

Subscribe to never miss an issue. Liquidity’s Daily Energy Market Updates provide a comprehensive analysis of both the fundamentals and technical factors driving energy markets.

Click below to view our other newsletters on our website:

Disclaimer

This article and its contents are provided for informational purposes only and are not intended as an offer or solicitation for the purchase or sale of any commodity, futures contract, option contract, or other transaction. Although any statements of fact have been obtained from and are based on sources that the Firm believes to be reliable, we do not guarantee their accuracy, and any such information may be incomplete or condensed.

Commodity trading involves risks, and you should fully understand those risks prior to trading. Liquidity Energy LLC and its affiliates assume no liability for the use of any information contained herein. Neither the information nor any opinion expressed shall be construed as an offer to buy or sell any futures or options on futures contracts. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Any opinions expressed herein are subject to change without notice, are that of the individual, and not necessarily the opinion of Liquidity Energy LLC

Reply